The Elusive Promise of Micropayments: A History of Unfulfilled Potential

Micropayments promised seamless, pay-as-you-go digital transactions—but why haven’t they taken off? From early visions to failed dot-com experiments and today’s renewed interest, we explore the obstacles holding them back and whether new technologies could finally make them viable. Is a revolution coming, or will subscriptions stay king?

Table of Contents

Where It All Started

During one of our usual Sunday afternoon coffees, We found ourselves in yet another debate about business trends. This time, we were venting about the hassle of managing multiple subscription services.

"Why does everything have to be a subscription?"

That question led to a deeper conversation. Were there better alternatives? Had businesses simply accepted this model without questioning it?

The discussion led us to explore micropayments - an old idea that we felt had been overlooked. We decided it was worth a closer look.

Brief History

What does "Micropayments" really mean?

Imagine you find an article online that interests you. You click on it, eager to read, but just as the first few sentences pull you in, a paywall appears. Your only option? A monthly subscription.

Frustrated, you close the tab and move on.

But what if you could simply pay a small amount to access just that one article? No subscription, no long-term commitment - just a quick, seamless transaction.

That’s the vision of Micropayments, a concept that has hovered on the edges of digital commerce for decades, yet never fully taken off. The question is, why?

To answer that question let’s take a closer look into the history of Micropayments, which I have divided into three phases.

Phase 1 - Origins and Early Vision (1960s–1980s)

The concept of micropayments itself was coined by Ted Nelson in the 1960s as part of his work on hypertext and digital copyright systems.

Nelson envisioned a decentralized network where fractional payments (as low as $0.0001) would automatically compensate creators for content reuse, enabling fair revenue distribution in collaborative works [1]. This idea, tied to his broader "TransCopyright" framework, aimed to embed payment metadata directly into digital content [2]. However, early networks like ARPANET and NSFNET (1980s) lacked commercial infrastructure, delaying practical implementation [2].

Phase 2 - The Dot-Com Era and Failed Experiments (1990s–Early 2000s)

In the 1990s, companies like IBM, Compaq, and startups such as Millicent, DigiCash, and Flooz tried to develop micropayment systems. IBM proposed hyperlinks that triggered payments, while Millicent used symmetric cryptography for sub-dollar transactions [1] [3]

The World Wide Web Consortium (W3C) even drafted HTML standards for micropayments, including tags like <price> and <duration> [1] [3]. Despite technical innovation, these systems failed due to:

- High transaction costs related to Credit Card fees

- User resistance - Consumers expected free content, and subscription/ad-based models dominated.

- Fraud and mismanagement: Companies like Flooz [2] collapsed due to money laundering schemes.

Phase 3 Renewed Interest and the Influence of New Technologies (Mid 2000s to Present)

Renewed interest in micropayments characterizes this phase, driven by the growth of digital content and e-commerce. New technologies such as instant payment systems and Distributed Ledger Technology (DLT) are being explored [4] and focus is on minimizing transaction costs and enhancing usability.

Despite the growing interest, a universally accepted definition of micropayments remains elusive, and many initiatives still face challenges. There is also debate about the feasibility of micropayments due to the mental transaction costs for consumers and competition from other payment systems [5].

Yet there is no company or organization so far that would achieve mainstream success.

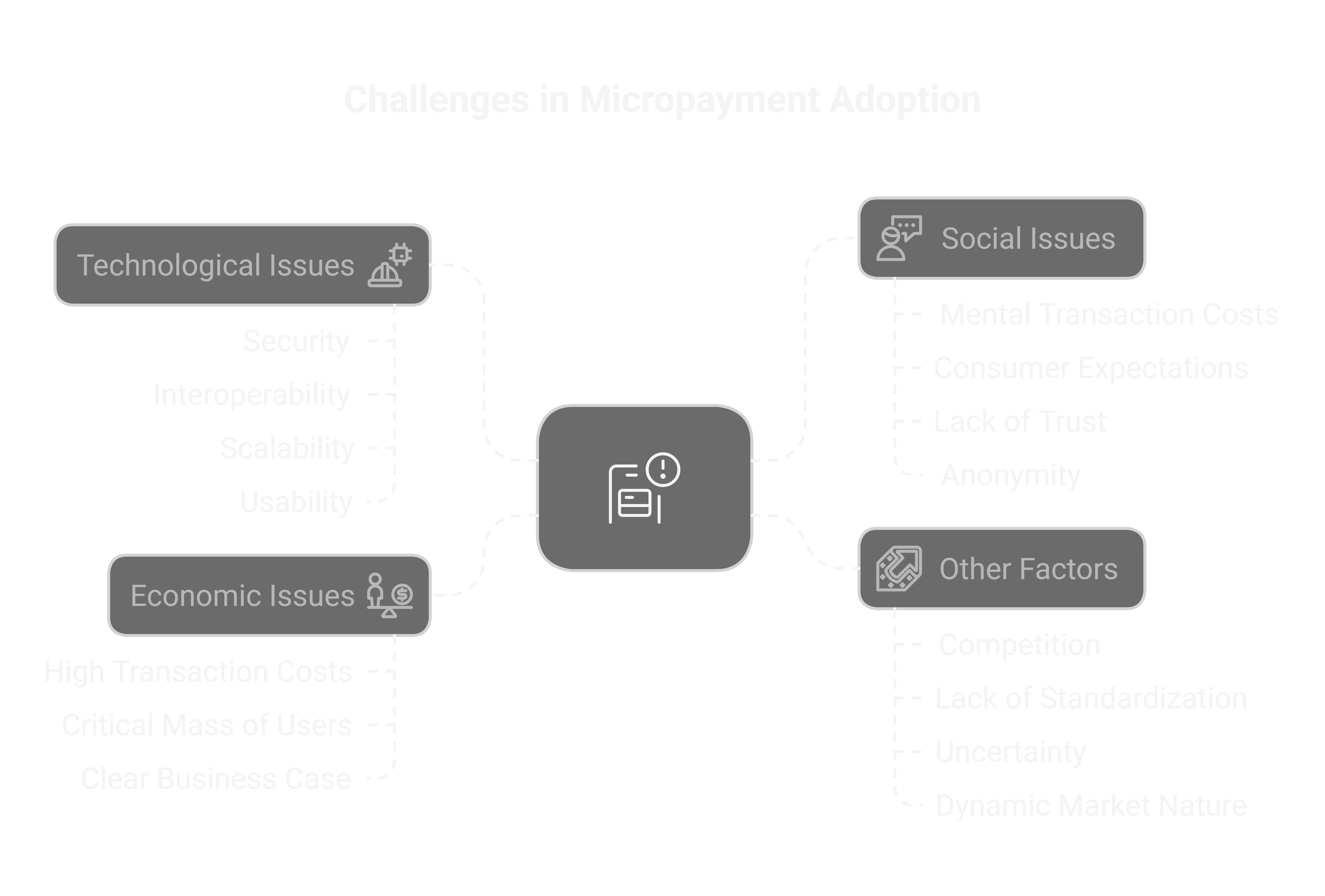

Challenges in Micropayments Adoption Overview

Understanding micropayments' history led us to a key question - What’s stopping their widespread adoption?

The main challenges fall into four categories:

Technological Issues:

Security is a primary concern. The underlying technology of micropayment systems must be secure to foster trust and prevent fraud. This includes the need for cyber-resilience and end-point security, particularly in e-commerce environments. [4]

Interoperability is essential for the smooth functioning of payment systems. A lack of interoperability between different systems makes it difficult for consumers to access payment accounts and for merchants to accept payments. The absence of interoperability has been a key reason why many micropayment solutions have failed.[4]

Scalability is another technological challenge. Micropayment systems need to handle large volumes of

transactions efficiently. This is particularly relevant with the growth of e-commerce, the Internet of Things (IoT), and the potential for autonomous peer-to-peer payments.[4]

Usability of the systems is also important. Systems that are complex or difficult to use can deter adoption. Micropayment systems should be simple, rapid, and easy to handle[6].

Economic Issues:

High transaction costs are a major obstacle. Traditional payment methods, such as credit cards, often have fees that make them unsuitable for very small transactions. Micropayment systems need to minimize transaction costs to be viable.[4]

The need for a critical mass of users is essential for the long-term viability of micropayments. Without enough consumers and merchants using the system, it will not be sustainable. Micropayment solutions need to be designed to meet the needs of both merchants and consumers to encourage adoption on both sides of the market.[4]

A clear business case must be apparent to both merchants and consumers. Merchants need to see a clear economic advantage to using a micropayment system, such as reduced transaction costs and access to new markets [6].

Social Issues:

Mental transaction costs are a significant barrier to consumer adoption. These costs refer to the effort consumers must make to decide if something is worth buying, regardless of its price [4]. Consumers may not want to spend time making numerous decisions for very small purchases [6].

Consumer expectations of free online content are also a challenge. Many consumers are accustomed to free online services and content, making them reluctant to pay even small amounts [4].

Lack of trust in new systems is another impediment. Consumers tend to be wary of new systems without an established positive reputation, especially when it involves handling their money [7].

Anonymity is often desired by consumers but is resisted by governments and sellers. While anonymity is seen as an advantage, sellers may want to avoid it to engage in price discrimination [8].

Other Factors:

Competition from other payment systems is a significant factor. Existing payment methods like credit cards and debit cards, as well as new methods like mobile payments or subscriptions, offer alternatives to micropayments [8].

Lack of a standardized system has also hampered the adoption of micropayments. The emergence of multiple proprietary systems has led to a lack of interoperability and user inconvenience.

Uncertainty about the demand and the constantly changing environment adds to the challenges for micropayments [4].

The dynamic nature of the market causes conditions to change frequently, requiring new solutions [6].

What's next for Micropayments ?

On the surface micropayments should be considered as a payments utopia - more of a dream or ideal rather than something that can be actually put into practice.

But is that really the case?

The landscape is shifting, and new technologies may finally remove the barriers that have held micropayments back.

Stay tuned for updates from the WDFT team, as we may have something that may actually address above road-blocks.

References:

1 - https://en.wikipedia.org/wiki/Micropayment

2 - Who killed the micropayment? A history.

3 - MicroPayments: A viable Business Model

4 - A big future for small payments? Micropayments and their impact on the payment ecosystem

5 - The effects of micropayments on online news story selection and engagement

6 - Micropayments - A Key To A Constrained Market